The article below is an excellent summary of modern central banking and it's involvement with economic wars. It leaves out some very important facts about its origins, which go back to Hjalmar Schacht, President of the Reichsbank and Minister of Economics under Adolph Hitler. The BIS was used to handle all the gold and assets stolen from pillaged countries, but I digress.

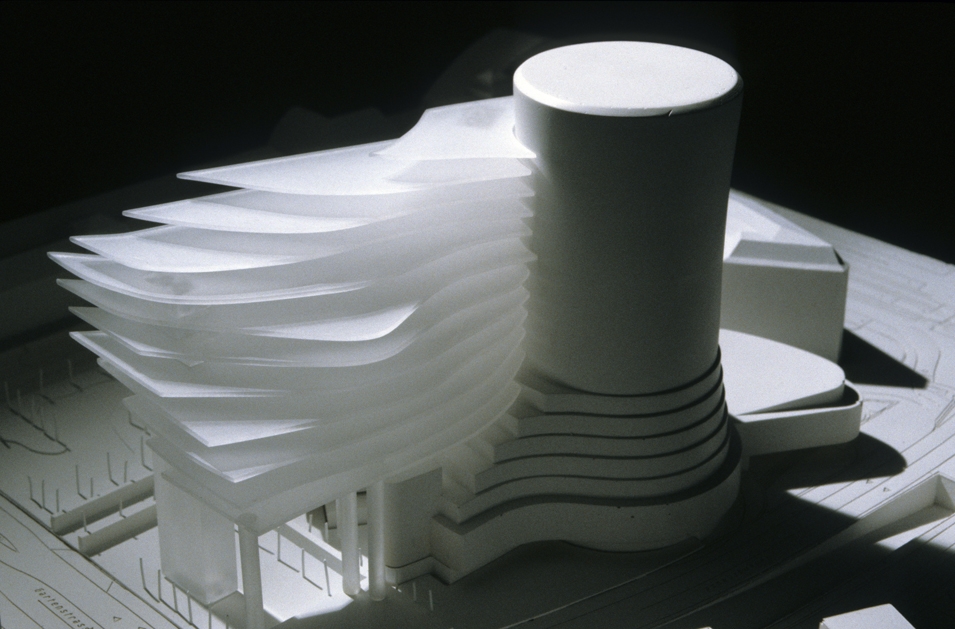

The Bank for International Settlements, otherwise known as the BIS, should more aptly be named the Bank for International division and domination. It's clearly an institution with global reach, whose hidden covert purpose is to impose the financial globalist's agenda on all sovereign nation states. The luminous photo below is of their luxurious Headquarters.

Ten times a year, once a month except in August and October, a small group of well dressed men arrives in Basel, Switzerland. Carrying elegant overnight bags and stylish brief cases, they discreetly check into the Euler Hotel, across from the railroad station. They come to this quiet city from places as disparate as Tokyo, Paris, Brasília, London, and Washington, D.C., for the regular meeting of the most exclusive, secretive, and powerful supranational club in the world.

Each visiting member has his own office at the club, with secure telephone lines to his home country. These elite international bankers are fully serviced by a permanent staff of about 300, including chauffeurs, chefs, guards, messengers, translators, stenographers, secretaries, and researchers. Also at their disposal are a brilliant research unit, well equipped medical facility and deep underground bunker, as well as a secluded country club with tennis courts and a swimming pool, a few kilometers outside of Basel.

Undoubtedly, we have all heard of this all important international organization, but how many of us really know much about it, or even understand its intended purpose. The only thing that I knew about this powerful global entity was that it is often described as the Central Bank of Central Banks. Clearly, we all need to know more, let's constructively begin with some benign elementary historical background transcribed from

Investopedia, and also lay out the venerable institution's specific functions & mission statement, directly from the BIS

website itself.

Founding and brief History of the BIS:

Founded in 1930, the Bank for International Settlements is the oldest global financial institution and operates under the auspices of international law. But from its inception to the present day, the role of the BIS has been ever-changing, as it adapts to the dynamic global financial community and its needs. The BIS was created out of the Hague Agreements of 1930 and took over the job of the Agent General for Repatriation in Berlin. When established, the BIS was responsible for the collection, administration and distribution of reparations from Germany - as agreed upon in the Treaty of Versailles.

After World War II, the BIS turned its focus to the defense and implementation of the World Bank's Bretton Woods System. Between the 1970s and 1980s, the BIS monitored cross-border capital flows in the wake of the oil and debt crises, which in turn led to the development of regulatory supervision of internationally active banks. More recently, it has concentrated its efforts on the global financial stability and capital reserve requirement accords. The BIS has also emerged as an emergency "funder" to nations in trouble, coming to the aid of countries such as Mexico and Brazil during their debt crises in 1982 and 1998, respectively. In cases like these, where the International Monetary Fund is already in the country, emergency funding is provided through the IMF structured program.

The BIS has also functioned as trustee and agent. For example, from 1979 to 1994, the BIS was the agent for the European Monetary System, which is the administration that paved the way for a single European currency. Today, the BIS has become the central bank of central banks. The Bank now represents the interests of nearly all of the world's central bank institutions, and manages a significant share of their reserves, including gold holdings. The organization now serves and presides over 60 central banks worldwide. Accordingly the BIS requires the capital/asset ratio of central banks to be above a prescribed minimum international standard, for the protection of all central banks involved.

The BIS has also functioned as trustee and agent. For example, from 1979 to 1994, the BIS was the agent for the European Monetary System, which is the administration that paved the way for a single European currency. Today, the BIS has become the central bank of central banks. The Bank now represents the interests of nearly all of the world's central bank institutions, and manages a significant share of their reserves, including gold holdings. The organization now serves and presides over 60 central banks worldwide. Accordingly the BIS requires the capital/asset ratio of central banks to be above a prescribed minimum international standard, for the protection of all central banks involved.

In broad outline, the BIS pursues its mission by:

- Promoting discussion and facilitating collaboration among central banks.

- Supporting dialogue with other authorities that are responsible for promoting financial stability.

- Conducting research on policy issues confronting central banks and financial supervisory authorities.

- Acting as a prime counterparty for central banks in their financial transactions.

- Serving as an agent or trustee in connection with international financial operations.

Now that we are up to speed on the BIS's alleged "raison d'etre", and fully indoctrinated in the organization's whitewashed history, self proclaimed mission statement and assumed functions, let's expose the true nature of this supposedly benign bastion of banking balance. Trust me, they are anything but the modest measured men of monetary moderation and management they purport to be. This odious institution is nothing but a conceited cunning cabal of carnivorous cannibals bent on global financial domination, who deftly deploy dreaded debt disbursements the world over. They will stop at nothing to achieve their ends, absolutely nothing.

To fully comprehend the self-serving nature of the BIS, one has to understand that it is an autocratic institution run by a very select group of the highest ranking bankers on the planet, representing both private banking interests, as well as those of the vast worldwide network of central banks that are ultimately owned by those same private commercial & financial interests. It is important to note that these top flight international bankers have intentionally organized themselves, so as not to be directed by their own national governments for the crucial decisions and actions they take. In effect, they are a supranational organization, controlled by an elite group of men, who preside over most of the world's financial and monetary systems of exchange which regulate and facilitate most of the globe's commerce.

The supreme inner club is made up of the half-dozen powerful central bankers at the apex of a privately devised international monetary system. Their dictate, which enshrines the inner club from the rest of the lessor BIS members, is the firm belief that central banks should act independently of their home governments. Their controlling organization is at the epicenter of global finance, and has inherently become increasingly connected and indispensable over time by design. A glaring early example of their self-serving grandiosity can be found in their despicable double dealings before the outbreak and during the hostilities of the World Wars.

The following passage, by well-respected financial historian Adam LeBor, details the nefarious activities of Thomas McKittrick, a former president of the BIS:

The BIS was founded in Basel in 1930, where it is still headquartered today. Ostensibly set up as part of the Young Plan to administer German reparations payments for WWI, its real purpose was detailed in its statutes: to “promote the cooperation of central banks and provide additional facilities for international financial operations.” The establishment of the BIS was the culmination of the central bankers’ decades-old dream to have their own bank powerful, independent, and free from interfering politicians and nosy reporters.

The BIS was founded in Basel in 1930, where it is still headquartered today. Ostensibly set up as part of the Young Plan to administer German reparations payments for WWI, its real purpose was detailed in its statutes: to “promote the cooperation of central banks and provide additional facilities for international financial operations.” The establishment of the BIS was the culmination of the central bankers’ decades-old dream to have their own bank powerful, independent, and free from interfering politicians and nosy reporters.

Under the terms of the founding treaty, the bank’s assets could never be seized, even in times of war. Most felicitous of all, the BIS was self-financing and would be in perpetuity. Its clients were its own founders and shareholders, the central banks. The BIS, boasted Gates McGarrah, an American banker who served as its first president, was “completely removed from any government or political control.” McKittrick’s involvement with the BIS began in 1931, when he joined the German Credits Arbitration Committee, which adjudicated disputes involving German commercial banks. One of the other two members was Marcus Wallenberg, of Sweden’s Enskilda Bank, who taught McKittrick about the intricacies of international finance. Marcus and his brother Jacob were two of the most powerful bankers in the world. During the war, the Wallenberg brothers used Enskilda Bank to play both sides and harvest enormous profits.

In May 1939 McKittrick was offered the position of president of the BIS, which he readily accepted. As head of the BIS, headquartered in Basel, from 1940 to 1946, McKittrick played a crucial role in abetting Hitler’s war—and, at the same time, in revealing details about his Nazi colleagues to his friends in Washington, D.C. On McKittrick’s watch, the BIS willingly accepted looted Nazi gold, carried out foreign exchange deals for the Reichsbank, and recognized the Nazi invasion and annexation of conquered countries. By doing so, it also legitimized the role of the national banks in the occupied countries in appropriating Jewish-owned assets. Indeed, the BIS was so indispensable to the overall Nazi project that the vice-president of the Reichsbank, Emil Puhl, who was later tried for war crimes, once referred to the BIS as the Reichsbank’s only “foreign branch.” In the closing months of the war, as American GIs fought their way across Europe, McKittrick was arranging deals with Nazi industrialists to guarantee their profits after the Allied victory.

In May 1939 McKittrick was offered the position of president of the BIS, which he readily accepted. As head of the BIS, headquartered in Basel, from 1940 to 1946, McKittrick played a crucial role in abetting Hitler’s war—and, at the same time, in revealing details about his Nazi colleagues to his friends in Washington, D.C. On McKittrick’s watch, the BIS willingly accepted looted Nazi gold, carried out foreign exchange deals for the Reichsbank, and recognized the Nazi invasion and annexation of conquered countries. By doing so, it also legitimized the role of the national banks in the occupied countries in appropriating Jewish-owned assets. Indeed, the BIS was so indispensable to the overall Nazi project that the vice-president of the Reichsbank, Emil Puhl, who was later tried for war crimes, once referred to the BIS as the Reichsbank’s only “foreign branch.” In the closing months of the war, as American GIs fought their way across Europe, McKittrick was arranging deals with Nazi industrialists to guarantee their profits after the Allied victory.

Additionally, the following indictment from Wikipedia:

As a result of Nazi collaboration allegations, at the Bretton Woods Conference held in July 1944, Norway proposed the "liquidation of the Bank for International Settlements at the earliest possible moment". This resulted in the BIS being the subject of a disagreement between the American and British delegations. The liquidation of the bank was supported by other European delegates, as well as the United States (including Harry Dexter White, Secretary of the Treasury, and Henry Morgenthau),[6] but opposed by John Maynard Keynes, head of the British delegation. Fearing that the BIS would be dissolved by President Franklin Delano Roosevelt, Keynes went to Morgenthau hoping to prevent the dissolution, or have it postponed, but the next day the dissolution of the BIS was approved. However, the liquidation of the bank was never actually undertaken.[7] In April 1945, the new U.S. president Harry S. Truman and the British government suspended the dissolution, and the decision to liquidate the BIS was officially reversed in 1948.

Fast forward to Today. Would the very same elite banking interests not be behind the destabilization and financing of multiple military conflicts sprouting up all over the globe? After all, the U.S. just finished squandering over $3 trillion endlessly tussling with a fanatical bunch of burka wearing nomads in the sparse mountains of Afghanistan for well over a decade. In the end, what, and who the hell was all of that money really for? Might it be supranational bank financing concerns funneling their central bank issued easy money government treasury funding directly into the military industrial complex.

MENA, after years of relative calm imposed by despotic regimes often legitimized by Western commercial interests, suddenly, all at once, seemingly out of nowhere, rose up in a spontaneous combustion of political awareness, the so called Arab Spring, which has brought as much disillusionment as promise. What was really behind this? While Syria, on the other hand, has been in a perpetual state of war due to ISIS insurgents supported by the U.S., Saudi Arabia, and Israel. Iraq is on the verge of complete disintegration as the same western organized ISIS move in on Baghdad. Libya is erupting, with American, British and French embassy's being swiftly evacuated. What gives? Are all of these simultaneous regional conflicts simply a sheer coincidence? Further war financing requirements perhaps.

The Hamas / Israel connection has certainly duped many, even though it is historical fact that the creation of Hamas itself was funded and supported by covert elements of the Israel government. Why did Israel put money and arms at the disposal of Muslim extremist groups like Hamas and ISIS, only to enter into brutal conflict with them later? Again, are the international bankers involved here as well? Why bother with inflation when you can create DeathFlation!

The Ukraine crisis is only further intensifying after the attack on Malaysian flight MH17. In just the past week, the EU has instituted serious economic and financial sanctions, fighting has become even more fierce in the ethnic Russian speaking regions, and Russia itself has been accused of firing heavy artillery into the war zone.

Moreover, the U.S. now claims that Russia has demonstrably violated the terms of the Intermediate Range Nuclear Forces treaty. Astonishingly, assistant Secretary of State, Victoria Nuland recently proudly trumpeted that U.S. sponsored NGOs (Non Governmental Organizations) had spent over $5 billion fomenting political protest on the ground in Kiev, in order to destabilize and ultimately overthrow the former president of Ukraine, Victor Yanukovych. Again, who or what institution actually facilitated the financing of such an excessive amount of funds, and why?

Is it simply the usual bane of proxy war profiteering which is underway, or is something more sinister also a foot here. Is the western central bank hegemonic monetary system attempting to further assert itself on the arising and defiant BRICS? Moreover, since all out military conflict is no longer a viable option, due to assured mutual destruction from imposing nuclear arsenals, another most effective avenue for global domination would be via strategic financial and economic power. Is this what the international banking cabal is now seizing upon?

A significant example of a BIS sponsored strategic global economic initiative, orchestrated by its self-serving megalomaniac banking power brokers, was its behind the scene’s role in devising and pushing forward the concept for a European Union with a single common currency. It established a new role for itself in the postwar world, first as the financial mechanism for American efforts to rebuild Europe, and then for the accelerating project of European unification. Some believe that the trans-national vision of a modern Europe ruled by mandarins in Brussels and Basel was originally hatched and concocted in a secret meeting held at the Bank for International Settlements.

Clearly, the driving force behind the financial engineering ambitions of the elite global bankers at the BIS has always been the same. Namely; to further establish themselves as the indispensable international financial body, whose ultimate authority supersedes any national jurisdiction, thereby interminably dismantling and diminishing the sovereignty of the individual nation states. In other words, they consolidate their subjugation of the local citizenry by championing the benefits of economies of scale which only globalization can achieve, and, of course, that only their financial frameworks can administer.

The UN, EU, NAU, IMF, WBC, CFR, NATO, WTO, OECD, WHO, and a myriad other IGOs (Intergovernmental organizations), all use much the same modus operandi as the BIS to expand their dominion. In the end, it's mostly about their self-seeking interests, entitled importance and institutional aggrandizement. Throughout history, elite groups of men have always attempted to subjugate the masses, this is no different. The once magnificent self determined Republic of the United States, for the people of the people, must stop these globalists dead in their tracks, before their self-serving hubris and unrelenting drive for hegemony brings unsuspecting Americans down to their knees.

Carroll Quigley, the renown academic historian, in his monumental tome

Tragedy and Hope published in 1966, clearly identified the underlying scheme of this scourge.

Having studied the rise and fall of civilizations, Quigley found the explanation of disintegration in the gradual transformation of social "instruments" into "institutions", that is, transformation of social arrangements functioning to meet real social needs into social institutions serving their own purposes regardless of real social needs.

Many discerning Americans are certainly aware of the prevalence of the false Left/Right paradigm in American politics which is clearly driven by the buying off of politicians via an army of private lobbyists on behalf of avaricious corporate institutions and demanding special interest groups. There is also a solid case to be made that our multinational banking institutions directly serve to promote this debilitating duplicitous demagoguery. The once esteemed news networks have also degenerated into a cronyism cesspool of unabashed corporatism, no longer reporting news, but rather dishing out distilled disinformation and various valueless vicissitudes. Institutional disintegration indeed, Mr. Quigley was flat out dead right back in 66'!

Professor Carroll Quigley directed his poignant prescient prose specifically at the Bank for International Settlements:

"The Power of financial capitalism had a far reaching plan, nothing less than to create a world system of financial control in private hands able to dominate the political system of each country and the economy of the world as a whole. This system was to be controlled in a feudalistic fashion by the central banks of the world acting in concert, by secret agreements arrived at in frequent meetings and conferences. The apex of the system was to be the Bank for International Settlements in Basel, Switzerland, a private bank owned and controlled by the world's central banks, which were themselves private corporations. Each central bank sought to dominate its government by its ability to control treasury loans, to manipulate foreign exchanges, to influence the level of economic activity in the country, and to influence co-operative politicians by subsequent rewards in the business world."

The ominous premise of this lengthy piece is precisely why the United States should become increasingly alarmed as these globalists continue to extend their supremacy. Just as the once proud independent self governing sovereign nation states of Europe have become subservient to an autocratic international banking class, which promptly imposed a common currency, and is now actively crafting a fiscal union to complete its ascendancy and authority, the United States also is a prime target in the cross hairs of these very same avaricious financial oligarchs.

Make no mistake, the likes of the BIS, IMF, IFC, OECD and the World Bank are on a maniacal maraudering mission to subvert the existing U.S. monetary system, via a crafty and cunning central bank, in our very own complicit Federal Reserve.

In my view, this is the only valid explanation as to why we are systematically being driven off a fiscal and monetary cliff, almost as if we were preforming a national financial and economic Hari Kari ritual. At this point, they have mandated a market cataclysm and deliberately determined the dollar's demise. To be sure, the BIS and IMF are waiting in the wings with a new global means of exchange based on an archetype of the presently established SDR mechanism.

Why else would the BIS be stating the following today regarding the FED's current monetary measures?

“The temptation to postpone adjustment can prove irresistible, especially when times are good and financial booms sprinkle the fairy dust of illusory riches. The consequence is a growth model that relies too much on debt, both private and public, and which over time sows the seeds of its own demise. To return to sustainable and balanced growth, policies need to go beyond their traditional focus on the business cycle and take a longer-term perspective – one in which the financial cycle takes centre stage…They need to address head-on the structural deficiencies and resource misallocations masked by strong financial booms and revealed only in the subsequent busts. The only source of lasting prosperity is a stronger supply side. It is essential to move away from debt as the main engine of growth."

Ask yourselves, if Janet Yellen sits on the Board of Directors of the BIS, why have she and all her 21st century predecessors been conducting a brazen, unproven, uncharted and surely precarious monetary policy with complete abandon, that totally contradicts the sage and proven advice, judiciously laid out above, by the very institution which is central to monitoring, regulating and advising on global central bank direction.

Something stinks here, it just doesn't add up. Is our Federal Reserve, whose top leadership also happens to be elite members of the BIS banking cabal club, actually double dealing here? Setting us up for a great fall, so the financial globalists can come sweeping in to our rescue, installing themselves as our monetary overlords? Far fetched, you say? Remember, this is well within their past predatory precepts, and typical of their self-serving Modus Operandi!

If we can't convince you, perhaps the view of billionaire hedge-fund legend Paul Singer will:

We were astounded to learn that the board of the BIS is comprised of none other than the heads of the major central banks of the developed world! Yes – Yellen, Draghi, et al! So, these central bankers are simultaneously failing to tell their respective governments that (1) monetary policy has done enough; (2) monetary policy is causing massive risks and distortions; and (3) political leaders must grab the reins and make structural changes, these same central bankers are authorizing BIS reports that will enable them to say, after the coming multifactor crisis, that they told us about the risks.

We wonder who from the Fed authorized the report, and why they haven’t shared these harsh views of Fed policy in the FOMC meeting minutes or the endless public speeches by Fed officials. It is duplicitous for the Fed to authorize the views in the BIS report yet keep quiet about them elsewhere. But then, the Fed has never accepted much responsibility for the 2008 crisis, despite its decisions to keep interest rates artificially low for an extended period of time, to do a poor job of regulating the banking system and to abet Fannie and Freddie in their utter irresponsibility. History rhymes. The Fed has created the fuel for another crisis, seems to know it judging by the BIS report, and yet is covering itself with an "I told you so" report from the BIS rather than changing course.

In closing, the following list identifies the current Board of Directors who preside over the Bank for International Settlements today, see if you recognize any of these supranational scoundrels.

The BIS Board of Directors:

Chairman: Christian Noyer, Paris Mark Carney, London Agustín Carstens, Mexico City Luc Coene, Brussels Jon Cunliffe, London Andreas Dombret, Frankfurt am Main Mario Draghi, Frankfurt am Main William C Dudley, New York Stefan Ingves, Stockholm Thomas Jordan, Zurich Klaas Knot, Amsterdam Haruhiko Kuroda, Tokyo Ann Le Lorier, Paris Stephen S Poloz, Ottawa Raghuram Rajan, Mumbai Jan Smets, Brussels Alexandre A Tombini, Brasília Ignazio Visco, Rome Jens Weidmann, Frankfurt am Main Janet L Yellen, Washington Zhou Xiaochuan, Beijing

The Globalists are indeed on the move...............