Tuesday, July 30, 2013

WHO FUNDS UN #AGENDA21/ SUSTAINABLE DEVELOPMENT?

Taken from http://www.democratsagainstunagenda21.com/who-funds-un-agenda-21.html

Growing Smart Legislative Guidebook Model Statues for Planning and the Management of Change was funded by grants from the US Department of Housing and Urban Development (the lead federal agency); Federal Highway Administration (US Department of Transportation); US Environmental Protection Agency; the Federal Transit Administration (DOT); the Rural Economic and Community Development Administration (US Department of Agriculture). All of these agencies were members of the President's Council on Sustainable Development which ran from 1993-1999.

Private funders included the Siemens Corporation; Henry M. Jackson Foundation; Annie E. Casey Foundation; and the American Planning Association. These private organizations promote smart growth.

Siemens, for instance, benefits from the development of the 'smart grid' and is a key private for-profit corporation for solar, biomass, and other subsidized power generation. This huge multi-national corporation is involved in health care, building systems, financing, communications and more. Siemens USA has revenue of over $20 Billion. They also just appointed Michael Kruklinski Head of Siemens Real Estate for the Americas. In this role he'll oversee all operations for Siemens Real Estate in the U.S. He also is on the NEW YORK CITY REGIONAL PLAN ASSOCIATION BOARD. Siemens is a German company that was nearly bankrupt until Hitler generously supplied free slave labor and money for technological development. http://www.usa.siemens.com/answers/en/

The Henry M. 'Scoop' Jackson (he sponsored the legislation to create the EPA) Foundation is a major grant funder. Their involvement on an international scale is detailed here:

The Foundation seeks to leverage its influence and effectiveness by convening and participating actively in groups of like-minded funders to discuss topics of mutual interest. Examples of funder partners or networks follow:

International Human Rights Funders Group

The Jackson Foundation is a founding member and former steering committee member of the International Human Rights Funders Group (IHRFG), an association of grantmakers dedicated to supporting efforts to protect human rights on both national and international scales. Members meet at least twice yearly to discuss issues of common concern in human rights philanthropy and reach out to potential funders to attract greater dollars to the human rights field. IHRFG also seeks to inform public policy on a national level. (text in italics is directly from the Jackson Foundation website--take a look at the funders)

The Funders' Network for Smart Growth

The Jackson Foundation is a founding member of the Funders' Network for Smart Growth and Livable Communities, a coalition that seeks to strengthen and expand philanthropic leadership and grantmaking that improves communities through better development decisions and growth policies. It brings together foundations, nonprofit organizations and other partners to address a range of environmental, social, and economic problems. (Text in italics is from The Funders' Network for Smart Growth website)

The Funders Network membership list is vast. Annie E. Casey Foundation is just one of many members. Read the membership list here: http://www.fundersnetwork.org/connect

We suggest that you look carefully at the members of the Funders' Network for Smart Growth and Livable Communities to see where the UN Agenda 21/Sustainable Development money trail leads. Money and power flow back and forth along these channels. Enterprise Community Development and LISC, for example, are on the list. They are for-profit affordable housing developers who benefit hugely from subsidies in smart growth and redevelopment (urban renewal) zones. Wal-Mart is a partner. The Orton Family Foundation is a partner. You'll find over 100 foundations and corporations on the list. Take a look. and look at this too, as an example of who funds the Smart Growth conferences.

On the issue of devaluation of property through regulatory means, we find it reprehensible that counties and cities recognize that development rights have value when they're being purchased in conservation easements, but they have no value when they're being taken away through regulations. You won't find many General or Comprehensive Plans that don't embed sustainable communities strategies in their elements. Most states require it by law through their legislation. These policies fund and support UN Agenda 21/Sustainable Development.

More and more non-profit organizations are being created, fragmenting from others, spinning off and creating more non-profits. Funding comes from state and federal grants, from your taxes and fees, private grants, donations (tax write-offs), and from lawsuits. You'll find the League of Women Voters advocating for Smart Growth. The Lung Association lobbies for Smart Growth. The National Association of Realtors advocates for Smart Growth. The Chamber of Commerce does too. So does the AFL-CIO. Are your dues or professional fees paying for UN Agenda 21/Sustainable Development. Are you volunteering for a group supporting UN Agenda 21/Sustainable Development?

SPEAK OUT. REFUSE TO PAY OR PAY UNDER PROTEST, AND TELL THE MEMBERSHIP WHY YOU ARE TAKING ACTION.

- See more at: http://www.democratsagainstunagenda21.com/who-funds-un-agenda-21.html#sthash.ovLYChLZ.dpuf

WHO FUNDS UN AGENDA 21/SUSTAINABLE DEVELOPMENT?

Growing Smart Legislative Guidebook Model Statues for Planning and the Management of Change was funded by grants from the US Department of Housing and Urban Development (the lead federal agency); Federal Highway Administration (US Department of Transportation); US Environmental Protection Agency; the Federal Transit Administration (DOT); the Rural Economic and Community Development Administration (US Department of Agriculture). All of these agencies were members of the President's Council on Sustainable Development which ran from 1993-1999.

Private funders included the Siemens Corporation; Henry M. Jackson Foundation; Annie E. Casey Foundation; and the American Planning Association. These private organizations promote smart growth.

Siemens, for instance, benefits from the development of the 'smart grid' and is a key private for-profit corporation for solar, biomass, and other subsidized power generation. This huge multi-national corporation is involved in health care, building systems, financing, communications and more. Siemens USA has revenue of over $20 Billion. They also just appointed Michael Kruklinski Head of Siemens Real Estate for the Americas. In this role he'll oversee all operations for Siemens Real Estate in the U.S. He also is on the NEW YORK CITY REGIONAL PLAN ASSOCIATION BOARD. Siemens is a German company that was nearly bankrupt until Hitler generously supplied free slave labor and money for technological development. http://www.usa.siemens.com/answers/en/

The Henry M. 'Scoop' Jackson (he sponsored the legislation to create the EPA) Foundation is a major grant funder. Their involvement on an international scale is detailed here:

The Foundation seeks to leverage its influence and effectiveness by convening and participating actively in groups of like-minded funders to discuss topics of mutual interest. Examples of funder partners or networks follow:

International Human Rights Funders Group

The Jackson Foundation is a founding member and former steering committee member of the International Human Rights Funders Group (IHRFG), an association of grantmakers dedicated to supporting efforts to protect human rights on both national and international scales. Members meet at least twice yearly to discuss issues of common concern in human rights philanthropy and reach out to potential funders to attract greater dollars to the human rights field. IHRFG also seeks to inform public policy on a national level. (text in italics is directly from the Jackson Foundation website--take a look at the funders)

The Funders' Network for Smart Growth

The Jackson Foundation is a founding member of the Funders' Network for Smart Growth and Livable Communities, a coalition that seeks to strengthen and expand philanthropic leadership and grantmaking that improves communities through better development decisions and growth policies. It brings together foundations, nonprofit organizations and other partners to address a range of environmental, social, and economic problems. (Text in italics is from The Funders' Network for Smart Growth website)

The Funders Network membership list is vast. Annie E. Casey Foundation is just one of many members. Read the membership list here: http://www.fundersnetwork.org/connect

We suggest that you look carefully at the members of the Funders' Network for Smart Growth and Livable Communities to see where the UN Agenda 21/Sustainable Development money trail leads. Money and power flow back and forth along these channels. Enterprise Community Development and LISC, for example, are on the list. They are for-profit affordable housing developers who benefit hugely from subsidies in smart growth and redevelopment (urban renewal) zones. Wal-Mart is a partner. The Orton Family Foundation is a partner. You'll find over 100 foundations and corporations on the list. Take a look. and look at this too, as an example of who funds the Smart Growth conferences.

On the issue of devaluation of property through regulatory means, we find it reprehensible that counties and cities recognize that development rights have value when they're being purchased in conservation easements, but they have no value when they're being taken away through regulations. You won't find many General or Comprehensive Plans that don't embed sustainable communities strategies in their elements. Most states require it by law through their legislation. These policies fund and support UN Agenda 21/Sustainable Development.

More and more non-profit organizations are being created, fragmenting from others, spinning off and creating more non-profits. Funding comes from state and federal grants, from your taxes and fees, private grants, donations (tax write-offs), and from lawsuits. You'll find the League of Women Voters advocating for Smart Growth. The Lung Association lobbies for Smart Growth. The National Association of Realtors advocates for Smart Growth. The Chamber of Commerce does too. So does the AFL-CIO. Are your dues or professional fees paying for UN Agenda 21/Sustainable Development. Are you volunteering for a group supporting UN Agenda 21/Sustainable Development?

SPEAK OUT. REFUSE TO PAY OR PAY UNDER PROTEST, AND TELL THE MEMBERSHIP WHY YOU ARE TAKING ACTION.

Here's a light rail train made by ....Siemens. Trains to nowhere that take decades longer than planned to build. You vote for a 1/2 cent sales tax and then you pay and pay and pay.

BREAKING!! Australian Politician Ann Bressington Exposes Agenda 21

Section I: Social and Economic Dimensions

Section II: Conservation and Management of Resources for Development

Section III: Strengthening the Role of Major Groups

Section IV: Means of Implementation

Just like in the late 1960's, the environmental movement has been hijacked. It is very possible that some of the funds from TARP and the Federal Reserve continue to finance the Club of Rome plan for a new world order. Watch this entire video and then look into Rosa Koire's interviews about her book "Behind the Green Mask" and her website http://www.democratsagainstunagenda21.com.

Monday, July 29, 2013

Federal Reserve is Desheeting Your Dollar into Worthless Toilet Paper #GlassSteagall #EndtheFed

When you feel as if your dollar doesn't go as far as it used to, remember the Federal Reserve prints money out of thin air and their charter member, primary dealer pals who own the Fed, are reducing your purchasing power.

Wolf Richter www.testosteronepit.com www.amazon.com/author/wolfrichter

Yet another reason to Reinstate #GlassSteagall and #EndtheFed.

Wolf Richter www.testosteronepit.com www.amazon.com/author/wolfrichter

While workers in the upper income categories, those who don’t have to worry about the price of toilet paper, have seen their incomes rise sharply over the years, the rest have been in a long downward spiral. To take just one measure: median household income, adjusted for inflation, has dropped 7.8% since 2000 (chart). The drop has been steeper for the lower income categories. These are the folks who do worry about the price of toilet paper. And for them, Kimberly-Clark Corp. and other tissue makers have a special strategy: “Desheeting.”

A word that top executives of personal-care conglomerates are proudly bandying about because it speaks of their corporate spirit of relentless innovation. And it cropped up during Kimberly-Clark’s second-quarter earnings call.

CFO Mark Buthman set the scene when he extolled “organic” sales growth of a whopping 3% in the second quarter, though actual sales, at $5.267 billion, were down fractionally year over year. A continuation of a worsening trend: in 2011, sales rose 5.5%. In 2012, sales rose only 1.0%, not even keeping up with inflation – a topic that came up a lot during the earnings call. In 2013, revenues look to be even more lackadaisical.

One exasperated analyst wanted to know with regards to the healthcare division, “Why do we have four quarters in a row of negative sales growth?”

“Yes. A couple of things,” retorted CEO Tom Falk, sticking to the rule of answering hairy questions with a yes; it would bamboozle everyone into having a positive attitude about the answer. “I think everybody in the healthcare space is trying to figure that out,” he said because his company wasn’t the only one with that problem. He ascribed it to high-deductible healthcare plans that encouraged consumers to make smart decisions; and to healthcare providers that pushed for “alternate therapies” before venturing into surgery. These efforts to tamp down on ballooning healthcare costs were giving his revenue-challenged company conniptions.

Yet Kimberly-Clark continues to eke out “adjusted earnings” growth – 8% per share in the second quarter. What gives? All manner of cost cutting, product-mix changes, and that word.

“Well, we took some desheeting in the quarter,” explained Mr. Buthman. The company was reducing the sheets on each roll of toilet paper and in each box of Kleenex. He called it an “innovation” that would lead to a “more positive” price. At the same time, volume, which the company counted in thousands of sheets, would decline. “Which net net, for us, works out to be a positive,” he said.

Citing the improved Cottonelle toilet paper line, he told an analyst, “It’s a great product, great category, growing rapidly. We will have to get you some, Connie, to try it.”

His strategy: “identifying and delivering cost savings in areas that our consumers and customers don’t care about....”

Because it’s tough out there. No revenue growth. Input prices that are increasing. Customers who can’t afford price increases. “Adjusted earnings” that have to increase. Solution: desheeting – rolls and boxes with fewer sheets. Consumers “don’t care about” that because they’re not supposed to notice.

Part of the innovation is to fluff up the tissue without adding more materials – 15% “bulkier,” it said on a box of Kleenex that had 13% fewer sheets in it, the Wall Street Journal discovered. In the Cottonelle line, sheet counts dropped by 5.7% to 9.6%. Fewer but fluffed up sheets, lower input costs for the company, and consumers who “don’t care about” that. A perfect solution – and a variation on an ancient theme – for hiding hefty price increases.

Other tissue makers are doing it too. They’re cutting the number of sheets per roll or box, they cutting the size of the sheets, and they’re fluffing up sheets to give consumers, as Mr. Buthman explained so eloquently in an interview, a “better, stronger, tissue so that you need fewer sheets to get the job done.”

But the math of getting “the job done” doesn’t quite work out that way. If someone for a particular “job” normally uses two sheets, he isn’t going to suddenly use 1.95 sheets for the same job to compensate for a 5% cut in sheet count, regardless of how fluffy and improved that innovative sheet may be. He’s going to use two sheets as before, and he’s going to buy more rolls and spend more money. If Kimberly-Clark’s cost-cutting and pricing strategy is working, he’ll never notice, though he might start wondering after a while where all his money is going.

Kimberly-Clark knows where his money is going. It’s propping up “adjusted earnings.” This is the high art of marketing to consumers who have been pauperized in small, nearly unnoticeable increments by over a decade of wage increases – for the lucky ones – that haven’t kept up with what the Fed is so passionate about creating: moderate inflation.

But the Fed has a problem. Foreigners have been big buyers of Treasuries. That buying collapsed during the financial crisis. Now, worried foreigners are once again bailing out. So far, the Fed has been picking up the slack. But what if the Fed were to “taper” those purchases, and long-term rates were to jump? Read.... Rising US Interest Rates Could Create An Economic Death Cycle. So Can The Fed Actually Taper QE?

Peter Schiff Discusses All the Reasons to Reinstate Glass-Steagall and End the Federal Reserve

Peter doesn't even mention Glass-Steagall because this is an old video, which is why his predictions are so impressive. If you listen to this interview closely, you will hear many good reasons to reinstate Glass-Steagall and end the Federal Reserve. I am not going to tell you what those reasons are. You will have to decide for yourself. Do the research. End the lies. Take America back from the stateless corporate fascist oligarchy that exerts massive power and influence over foreign and domestic policy!

@TwistedPolitix: Peter Schiff Discusses All the Reasons to Reinstate #GlassSteagall and #endthefed http://t.co/1uvfebUQE8 #NWO

— #GlassSteagall? (@TwistedPolitix) July 29, 2013

SIGN/RT: Join @SenWarren in calling for a new #GlassSteagall Act to restore sanity to Wall Street: http://t.co/baytPcEnET #p2 @CREDOMobile

— White Oval (@jimgzmail) July 29, 2013

Mine is signature 113,188 on this Petition to Reinstate the Glass-Steagall Act http://t.co/WfxCB9q1as via @moveon #GlassSteagall

— Sarah Reynolds (@Sarah__Reynolds) July 26, 2013

Friday, July 26, 2013

What's the connection between the Federal Reserve, Too Big to Fail, and Glass-Steagall?

What's the connection between the Federal Reserve, Too Big to Fail, and Glass-Steagall?

Ron Paul: Foreign Policy & Israel

This is why you should have voted for Ron Paul and Jesse Ventura in 2012. We would be lucky if we had that chance again in 2016.

Congressional Stalling Tactics While Working for Banks #GlassSteagall #DoddFrank

They are stalling! Reinstate Glass-Steagall NOW before it's too frickin late!

Barney Frank dismisses calls for Glass-Steagall redux

{kind=link}

How Liberty-Minded Individuals Can Fight UN #Agenda21

#BundyRanch is preview of #Agenda21 and Club of Rome plans for "sustainable growth" through depopulation and... http://t.co/5r2m7PxPAk

— Conservative Freaks (@Freak1791) April 12, 2014

Thursday, July 25, 2013

Adding Insult to Injury, Larry "Pull It" Silverstein, and the 9/11 Terrorist Attacks

Billions of dollars of gold deposited underneath the World Trade Center complex went missing after 9/11. Hmm. The rest of the building apparently disentegrated and fell at near freefall speed, collapsing in less than 10 seconds from start to finish, and a billion dollars gold evaporated in a freak alchemist experiment, or was shipped off to China with the scrap metal by Giuliani, or it was stolen the morning of the 9/11 attacks just before the planes hit. Smart burglers?

Why is no one claiming their gold? Are they afraid to question the official word of the mighty United States? The country with the world's largest military, a country that is recognized by its own population as an evil empire manipulated by an elite oligarchy loyal to the Queen of England, the Pope, and Lucifer? I guess the official answer is B), in which case we need to arrest Giuliani, because he is clearly a guilty bastard!

Then there's this Silverstein guy.

Now, 12 years later and he is at it again. This time sueing the airlines and making a claim on his commercial property insurance, with whom he had negotiated terrorist coverage months after he bought the place and months before 9/11. How convenient. And now he wants more money? Guilty greedy bastard!

WTC7 Owner Larry Silverstein Sues Airlines for Billions Over 9/11 After $5 Billion Insurance Payment http://t.co/wXY6mFCIuG

— #GlassSteagall? (@TwistedPolitix) July 26, 2013

See these articles from Insurance Journal, THE premier insurance news site for the industry.

Silverstein Denied Right to Seek $3.5 Billion From Airlines

Real estate developer Larry Silverstein was denied the right to seek $3.5 billion from airlines whose planes were hijacked by terrorists and flown into the World Trade Center’s twin towers on Sept. 11, 2001. U.S. District Judge Alvin K. Hellerstein …

New York Judge to Rule If WTC Developer Can Seek Damages From Airlines

A federal judge is days away from deciding if New York developer Larry Silverstein can recover as much as $3.5 billion from airlines for damages to the World Trade Center on Sept. 11, 2001, on top of more than $4 …

Judge to Mull If Airlines Owe WTC Owners Over 9/11

A judge who has presided over most of the litigation stemming from the Sept. 11, 2001, terrorist attacks will decide whether the owners of the World Trade Center can try to make aviation companies pay billions of dollars in damages. …

World Trade Center Developer Challenges Airline’s ‘Act of War’ Defense for 9/11 Attacks

The leaseholder of the World Trade Center properties is asking a U.S. federal judge to reject arguments that American Airlines is not liable for damages stemming from the Sept. 11, 2001 hijackings because the attacks were an act of war. …

United Airlines Not Liable for Alleged 9/11 Security Lapse: Judge

United Airlines bears no responsibility for suspected security lapses at a Maine airport, which allowed hijackers to board the American Airlines plane that crashed into one of the World Trade Center towers on Sept. 11, 2001, a federal judge ruled. …

Inflation is MUCH higher than reported by government!

Submitted by Charles Hugh-Smith of OfTwoMinds blog,

Purchasing power and exposure to real costs are more realistic measures of inflation than the consumer price index.

That the official rate of inflation doesn't reflect reality is easily intuited by anyone paying college tuition and healthcare out of pocket. The debate over the accuracy of the official consumer price index (CPI) and personal consumption expenditures (PCE--the so-called core rate of inflation) has raged for years, with no resolution in sight.

The CPI calculates inflation based on the prices of a basket of goods and services that are adjusted by hedonics, i.e. improvements that are not reflected in the price of the goods. Housing costs are largely calculated on equivalent rent, i.e. what homeowners reckon they would pay if they were renting their house.

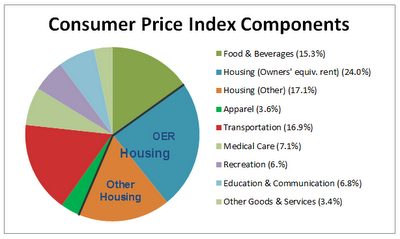

The CPI attempts to measure the relative weight of each component:

Many argue that these weightings skew the CPI lower, as do hedonic adjustments. The motivation for this skew is transparent: since the government increases Social Security benefits and Federal employees' pay annually to keep up with inflation (the cost of living allowance or COLA), a low rate of inflation keeps these increases modest.

Over time, an artificially low CPI/COLA lowers government expenditures (and deficits, provided tax revenues rise at rates above official inflation).

Those claiming the weighting is accurate face a blizzard of legitimate questions. For example, if healthcare is 18% of the U.S. GDP, i.e. 18 cents of every dollar goes to healthcare, then how can a mere 7% wedge of the CPI devoted to healthcare be remotely accurate?

Those claiming that the CPI is more or less accurate point to the inflation rate posted by The Billion Prices Project @MIT as real-world evidence. The Billion Prices Project collects real-world prices from online retailers for thousands of goods. The Project's rate of annual inflation closely tracks the official CPI, though recently it has diverged, climbing above 2.5% annually while the CPI is below 1.5%.

The fatal flaw in The Billion Prices Project is that it does not track the real-world cost of big-ticket services such as healthcare or tuition that dominate household budgets for those who have to pay for these services.

Those claiming the CPI grossly underestimates inflation often compare the current CPI with the CPI methodology of the 1980s. Using the old methodology, inflation is more like 9% rather than 1.5%.

Critics of this comparison claim the old methodologies were flawed and the new method is statistically superior.

Another way to track inflation is via households' actual spending as reflected in their budgets. Intuit collects anonymous spending data from 2 million users of Mint.com and posts the results: Presenting Inflation... the rise in expenses 2011 - 2013 (Zero Hedge). This data suggests the cost of daycare, healthcare insurance, kids' activities and tuition have skyrocketed in the past few years, making a mockery of the official annual inflation rate of 1.5% to 2%.

Chartist Doug Short recently published this graph plotting college tuition, medical care and the cost of a new car. According to the Bureau of Labor Statistics Inflation Calculator, $1 in 1980 = $2.83 in 2013. For example, the average cost of a new car in 1980 was $7,200, so the inflation-adjusted price in 2013 would be $20,376. The actual average price today is around $31,000, so after adjusting for inflation the current average price of a new car is higher than in 1980.

This chart reflects the real increases in cost:

In my analysis, the debate over inflation misses two key points. What really matters is not the rate of inflation, which can be endlessly debated, but the purchasing power of earned income, i.e. wages.

Instead of fruitlessly arguing over hedonic adjustments and the weighting of components, we should ask: how many hours of labor (at the average hourly rate for full-time workers) does it take to buy a loaf of bread, a new car, a gallon of gasoline, a new TV, a new house, college tuition and fees, etc., and compare that to how many hours of labor it took to buy all those goods and services in the past.

This methodology eliminates hedonics (i.e. the computer you buy today is much faster than the one you bought 10 years ago), as this adjustment plays no part in the actual costs of manufacture or the consumer's decision: we don't have a choice to buy a computer with 1990-era specs, so the hedonic adjustment is merely a tool for gaming the CPI.

We should also recognize that the experience of inflation differs in each economic class. Government employees who pay a small percentage of their real healthcare insurance costs (or none at all) will experience little of the actual inflation in healthcare costs; it's the government agencies that are exposed to the real costs of healthcare insurance, which is why municipalities and agencies exposed to the skyrocketing costs of healthcare insurance are under financial pressure.

A retiree is naturally focused on the out-of-pocket share of medication costs; the soaring cost of college tuition is so remote it might as well be occurring on Mars.

Consider this real-world example. Let's say a household earning $60,000 a year (median household income is around $50,000) is suddenly exposed to the real cost of rising healthcare insurance. Maybe the primary wage earner lost the job that provided health coverage and now has to pay the full costs out of pocket as a contract worker.

In any event, their healthcare insurance now costs $500 more per month than it did last year. (By happenstance, this is how much my own healthcare insurance costs have risen since 2008.) This $500/month means the household is paying $6,000 or 10% of its gross income more for the same coverage it received last year. The household's annual rate of inflation just from healthcare costs is 12%, since net income is closer to $50,000 and the $6,000 in extra spending isn't buying any new good or service.

Let's say the household is paying $500 more per month for healthcare insurance than it was five years ago. That works out to an annual rate of 2.4% just from healthcare insurance inflation alone. Any other increases in costs would push that rate higher.

In other words, those households with zero exposure to college tuition and the full costs of daycare, medical care and healthcare insurance may well experience low inflation, while the household paying the full costs of daycare, college tuition and healthcare insurance will experience soaring inflation.

If we analyze inflation by purchasing power (which declines as real income stagnates and prices rise) and by exposure to real costs, we find the incomes of the upper 5% have typically outpaced CPI inflation, so the purchasing power of the high-income family has not suffered (unless of course they have no healthcare insurance and they have to pay the full real costs of a medical crisis. In that case they might be bankrupt.)

Households that receive multiple government subsidies and direct payments have little exposure to healthcare, since they are covered by Medicaid, and modest exposure to housing if they receive Section 8 benefits. Retirees on Medicare also have limited exposure to the real-world costs of their care paid by the government.

If we analyze inflation by these two metrics, we find the middle class is increasingly exposed to skyrocketing real-world prices. Pundits in the top 5% have the luxury of pontificating on the accuracy of the CPI while those protected by government subsidies and coverage have the luxury of wondering what all the fuss is about. Only those 100% exposed to the real costs experience the full fury of actual inflation.